By The Searchlight Editorial Team / June 12, 2026

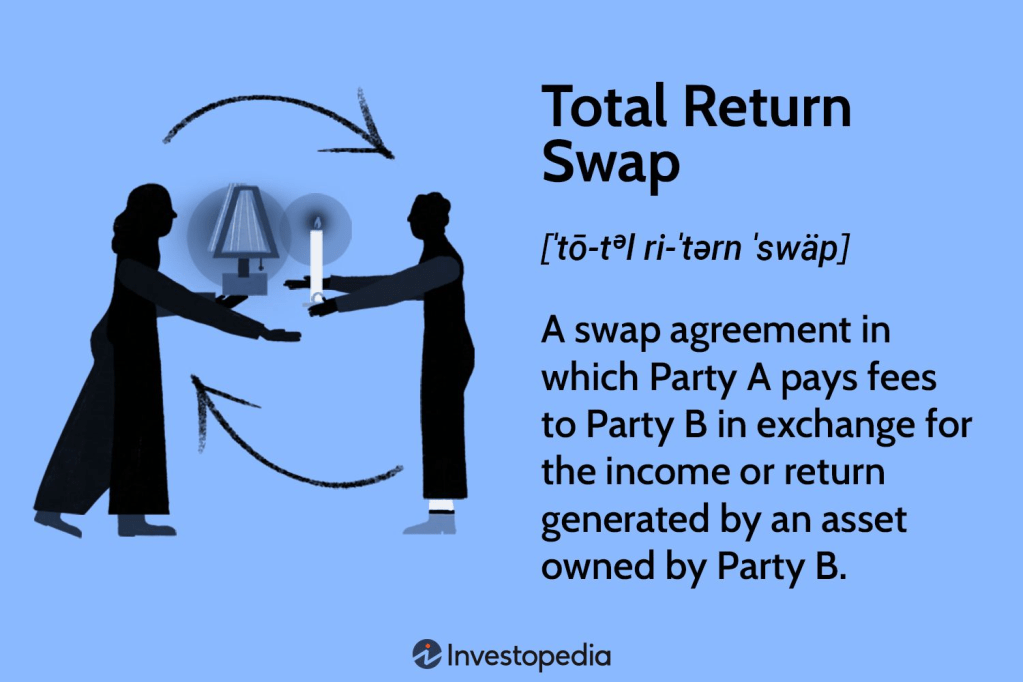

This TSR loan is from a bank in Abu Dhabi, the middle east and it is not a conventional loan. It is a derivatives-based structured financing deal. Nigeria would receive upfront dollars (in tranches) by effectively transferring the total economic returns (interest, price appreciation/depreciation, etc.) on underlying Naira-denominated sovereign securities or bonds to the bank. The securities serve as collateral, often over-collateralized (e.g., 133% or more of the loan value).

In exchange for the cash, the bank receives the “total return” on those assets. The structure allows Nigeria to access liquidity for refinancing expensive debt and funding infrastructure while potentially recording it in ways that defer full immediate debt recognition (though it creates contingent liabilities and margin obligations). Nigeria’s Senate has approved the plan.

The IMF Is Discouraging It?

The IMF has explicitly cautioned Nigeria against this deal, highlighting several risks during its 2026 Article IV consultation briefing. Key concerns from IMF officials like mission Chief Christian Ebeke include:

– Opacity and complexity: The Total Return Swap deals are often not fully transparent. The terms can be hard for stakeholders (including the public, parliament, and even the IMF) to assess, making it difficult to evaluate true fiscal implications, costs, and risks.

– Financial risks: They can expose the borrower to hidden costs, market volatility, and margin calls (additional cash or collateral demands if the value of the underlying securities falls). This has already caused issues elsewhere.

– Debt sustainability and transparency: While providing short-term relief, such instruments can complicate debt management, create contingent liabilities, and undermine efforts toward sustainable borrowing. The IMF generally prefers more straightforward financing amid Nigeria’s reforms, which have improved market access.

The IMF acknowledges Nigeria’s recent economic reforms and better stability but urges caution with these “innovative” structures.

Which Countries Have Taken TRS Deals?

Nigeria is following a trend among African nations seeking alternatives to high-cost traditional bonds or constrained IMF/ multilateral financing, especially amid global rate pressures and geopolitical events (e.g., conflicts affecting yields).

– Angola: Entered a ~$1 billion (split into tranches) one-year TRS with JPMorgan in late 2024/early 2025, using newly issued Eurobonds as collateral. It faced a significant ~$200 million margin call in 2025 due to market moves, highlighting volatility risks. Angola has used the loan for liquidity while managing debt recording nuances.

– Senegal: Engaged in multiple TRS deals (e.g., seven in 2025 totaling around $1.3 billion equivalent, including ~€650 million with entities like Africa Finance Corporation and FAB). It used the deals for bridging financing needs amid debt pressures and to avoid or delay restructuring. Costs were reportedly lower than bonds in some cases but still carried margin and transparency issues.

Other mentions include explorations by countries like Gabon or broader use of non-standard financing in Africa. This reflects a pattern of “financial engineering” for liquidity in resource-constrained or high-yield environments, but with recurring concerns about hidden or contingent debt.

Implications of the deal for Nigeria, Especially Amid Ongoing Borrowing Under President Tinubu

Nigeria’s debt has grown substantially under the Tinubu administration (since May 2023). When Tinubu took office, the total public debt was around ₦87 trillion (as of Q2 2023). By late 2025/early 2026, it reached approximately ₦152–159 trillion (with variations by reporting date and exchange rates), driven by naira devaluation, new borrowings (domestic and external), and fiscal needs.

Critics note that new borrowings in the first ~2 years exceeded historical accumulations in nominal terms, with debt servicing consuming a large share of revenues (projected high in 2026 budgets). The government highlights revenue increases, reserves, and reforms (e.g., fuel subsidy removal, Forex unification) as context, alongside infrastructure and deficit financing needs.

Potential benefits of the TRS are:

– Lower effective borrowing costs than current expensive domestic or international markets.

– Quick dollars for infrastructure and refinancing.

– Alternative to traditional loans/bonds amid elevated global rates.

However, the risks and implications are:

– Margin calls and volatility: If Naira securities or markets decline, Nigeria could face sudden additional dollar payments, straining reserves or forcing more borrowing/sales (as seen in Angola).

– Debt burden and servicing: Adds to overall liabilities (even if structured as derivatives). With existing high debt service (often >50% of revenues in projections), it could crowd out spending on health, education, and capital projects. Naira devaluation inflates local-currency debt figures.

– Transparency and governance: Opaque terms raise accountability issues. Nigerians deserve full disclosure of costs, collateral details, risks, and how funds will be used/audited to avoid “hidden debt” pitfalls.

– Long-term sustainability: Compounds reliance on external financing. IMF and analysts warn of cycles if not paired with revenue diversification, fiscal discipline, and growth. Positive reforms exist, but debt-to-GDP and per capita burden remain concerns (e.g., hundreds of thousands of Naira per citizen).

– Broader context: Nigeria has repaid past IMF loans (e.g., $3.4B COVID facility) but continues engaging multilaterals. Shifting to such swaps may signal diversification but also higher-risk strategies.

Overall, while offering short-term breathing room, the TRS fits a pattern of escalating debt under fiscal pressures. Nigerians should demand rigorous parliamentary oversight, independent analysis of full costs/risks, and a clear strategy linking borrowings to productive investments and debt reduction. Without strong execution, it risks exacerbating vulnerabilities in an oil-dependent economy facing inflation, poverty, and global headwinds. Transparency and prudent management are essential for public trust.

It is necessary to understand the Total Return Swap (TRS) is a financial derivative contract between two parties that allows one party to gain the economic benefits (and risks) of owning a reference asset without actually purchasing or holding it on their balance sheet. It is essentially a way to exchange the total economic performance of an asset for a periodic financing payment.

Core Parties in a TRS

– Total Return Payer (often the asset owner or bank in sovereign deals): Pays the total return of the reference asset to the other party. This includes income (interest, dividends, coupons) + capital gains or losses (price appreciation or depreciation).

– Total Return Receiver (the “investor” or, in sovereign cases like Nigeria, effectively the borrower/government): Receives the total return but pays a floating or fixed financing rate on a notional amount.

The payer typically retains legal ownership of the asset, the Eurobond but transfers its economic risks and rewards synthetically.

The Searchlight is coming with Part 2 to explain the TRS Agreements.

Leave a comment